Welcome to

The Re-Generation

Why Chrysalis?

Our Intention

To regenerate underutilised and degraded land by enhancing its ecology, meeting local social and development needs, with local partners, and producing a strong economic return.

What’s different about our approach?

Under-utilised land is often overlooked, yet is readily available.These sites offer multiple potentials, ‘low’ baseline for nature- based solutions and development.

Why now?

The degraded state of nature overall - aligned with BNG and UK Net Zero obligations.

Investment at scale is becoming available for nature-based solutions.

Coupled with increasing investor confidence - evolving market maturity for Biodiversity units and CO2e.

Opportunity to apply regenerative mindset to realise the full potential and breadth earth impacts vs narrow carbon or BNG only focus.

Our focus is on the following 3 pillars

Under-utilised Land

low base / high potential

Assess degraded land and establish a clear baseline for regenerative improvement

Regenerative Thinking

multiplier effect

Use regenerative design to implement improvements and reverse the ecological spiral

Dashboard Reporting

clear / transparent

Transform land and deliver a perpetual

economic and regenerative return

The current UK landscape provides a compelling market environment for Chrysalis to accelerate earth impact benefits.

Underutilised Land - can be improved from a low base – low value/seen as liability provides opportunity. Secured through known parties through partnerships and acquisitions.

Brownfield - a New Asset class emerging in strategic land market.

Established ESG Land – market competition is increasing land price for “protected” or already “enhanced” land with narrower margin for future improvements.

Market – fragmented but rapidly changing, opportunity to be at the forefront. Real estate sector slow to respond and have challenged new targets.

Built environment – main politics parties both support 200 – 300k new homes p.a. opportunity to balance the environment built environment to enable support from government, local authorities, communities, Investors & developers.

Experience – market is mature to deal with all kinds of land and challenges from title, environmental issues and tenure. We can bring all this together.

Reporting – evolving as companies and industry adopt different metrics or are developing different metrics in different sectors eg Future Homes task force.

The Market

Our aim is to continue to be at the forefront

and an influencer in these emerging markets.

• Increased market activity

driven by ESG corporate and

legal requirements

• Revenues driven through BNG

and flood management

• Demand for greater reporting

transparency and avoiding

greenwashing

• Market competition increasing

for greenfield land

• Regulatory and investor pressure

on offsetting impact on real

estate developments

• Opportunity to diversify revenues

across asset e.g. Social benefits

Voluntary nature-based

carbon markets

• Woodland Carbon Code

• Peatland Code

• Hedgerow Carbon Code

• UK Saltmarsh Code

• Farm Soil Carbon Code

Compliance nature-based markets

• Biodiversity Net Gain

• Nutrient credits

• S106 planning requirements

– NN/BNG

• Phosphate and Nitrate

pollution prevention credits

(LPA requirement)

Voluntary water and flood risk markets

• Phosphate credits

• Wetland, arable reversion

and cover crops

Emerging markets

• Green social prescribing

• ESG indicators

Emerging markets

• 219 Projects

• 177 Place-based or Sub-regional

Projects

• 42 ‘Enabler’ Projects (national or

regional bodies)

• 16% of Projects reported relate

to Urban Habitats (no statistics

on brownfield sites)

Voluntary nature-based

carbon markets

In total, as of 31 March 2023, 24,344ha of woodlands have been validated and verified under the Woodland Carbon

Code, according to interim data from the WCC, up from 18,500 a year earlier.

Source: Forest Research

Our Approach

Reversing the ‘Degenerative’ spiral

Our regenerative approach considers all characteristics of the land and surroundings to realise the maximum potential of the site.

Our goal is to intervene in the early stages of the under-utilised land and accelerate improvements and benefits through investment, the return on investment is then

measured from a financial, social and environmental perspective.

We can demonstrate clear direct benefits and improvements which can then be used to support external companies’ targets, balance any built environment on or off site or in return for financial contributions.

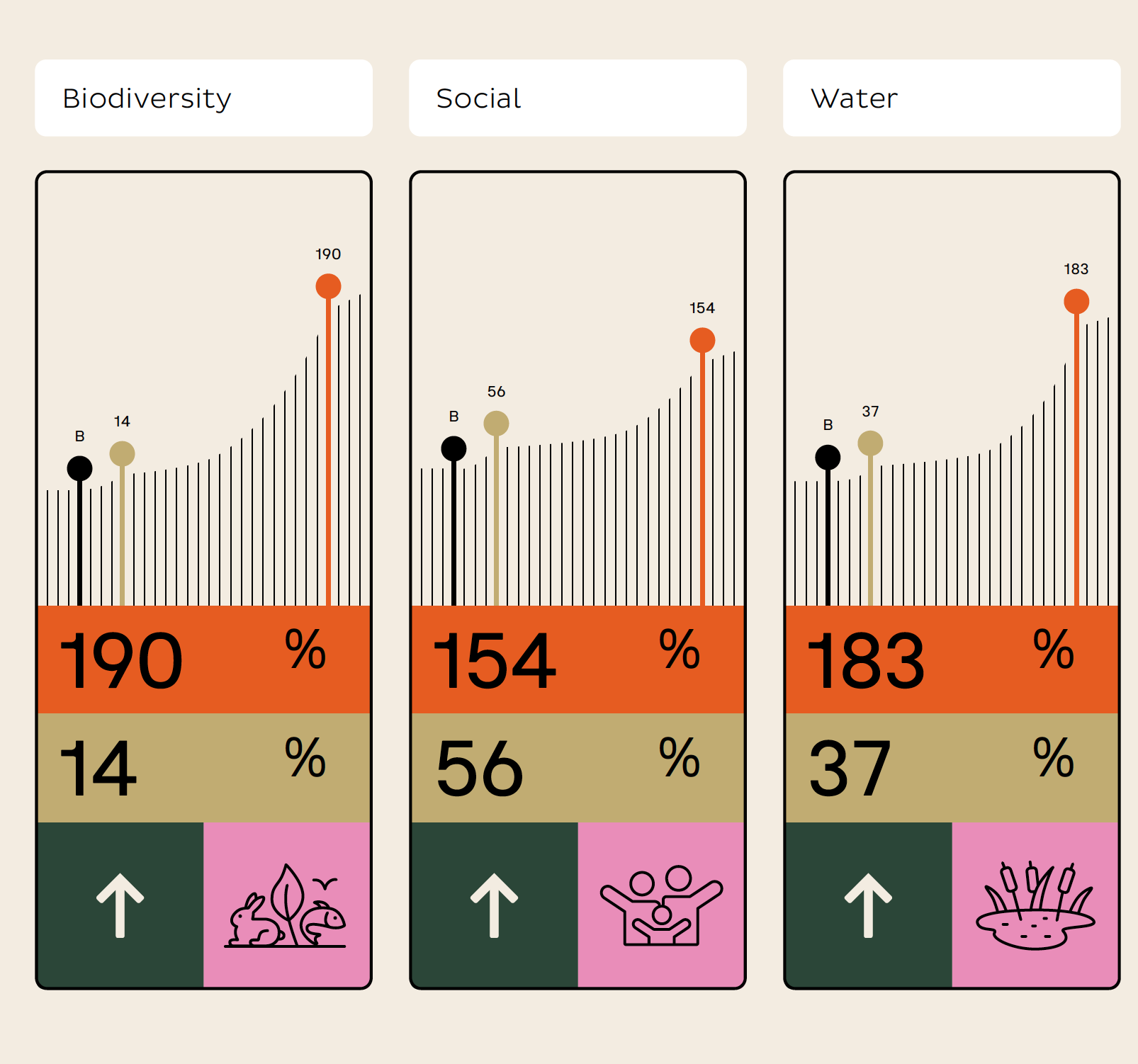

Regenerative Reporting

The Chrysalis Dashboard

Each element of our reporting supports and reinforces the other, achieving multiple benefits, enabling the potential of each asset

to be realised.

Our regenerative reporting covers each characteristic as follows:

BASE initial measured assessment of the site

CURRENT annual assessment and current position

TARGET the initial target for improvement

SUMMARY an overall indicator as to how each site is performing

Asset Case Study

The Regeneration Team

Our team has a blend of experience and skills in the environmental, built environment and corporate environments.

Accelerated transition towards regenerative futures.

Global mindset towards investing and developing real estate.

Large investment portfolio management.

Experience in managing sourcing and transaction of land assets.

Ajay Arora is an investment Manager

with experience

in Real Estate and Banking in UK and Australia.

Simon Bailey leads

LSP Leadership, who are about building confidence,

courage and conviction in leaders to take action.

Kevin Moriarty has over

30 years’ real estate

experience managing

large scale investments in senior leadership positions across Europe.

Nathan Nelson has over 25 years of experience in helping organisations

communicate, collaborate and deliver their projects effectively.

Rob Draper is experienced in transactions involving strategic land

throughout the UK.

Contact Chrysalis

All enquiries from prospective

investors should be directed to: